Most founders build a financial model when an investor asks for one. For a bootstrapped startup, that is the wrong instinct at the wrong time.

When your business runs on internally generated revenue with no venture capital, no seed round, no safety net a financial model is not a pitch document. It is the operating system of your company. It tells you when you can hire, when you must pause, and how long you can survive if growth stalls for 60 days. Building it late is not just a planning failure. It is a survival risk.

This guide explains exactly what startup booted financial modeling is, how it differs from every other type of startup financial model, and how to build one that drives real decisions rather than collecting dust in a Google Drive folder.

Table of Contents

What Is Startup Booted Financial Modeling?

Startup booted financial modeling commonly written as bootstrapped financial modeling is the discipline of forecasting a startup’s financial future using only internally generated revenue, founder capital, and early customer payments as the funding engine. No assumed future funding rounds. No hypothetical capital injections. Every projection begins with what the business can actually earn.

The term “booted” is shorthand for “bootstrapped” a startup that grows without external equity investment. The financial model built for this context prioritizes cash survival, break-even discipline, and revenue-funded growth over valuation optimization or investor-friendly hockey-stick projections.

The core contrast is structural:

| Dimension | Venture-Backed Financial Model | Bootstrapped Financial Model |

|---|---|---|

| Primary funding assumption | Future capital rounds | Revenue and retained earnings |

| Growth philosophy | Blitzscaling — capture share first | Sustainability — cash covers growth |

| Error tolerance | High (investors can inject capital) | Low (cash gaps can kill the business) |

| Projection horizon | 3–5 years | 12–18 months with 90-day precision |

| Primary metric | Valuation and ARR growth rate | Cash runway and contribution margin |

| Model purpose | Raise money | Run the business |

That table is not a judgment call about which approach is better. Companies like Mailchimp, Basecamp, and Spanx grew to hundreds of millions in revenue without venture capital. Companies like Uber and Airbnb needed massive external funding to achieve their specific market dynamics. The model must match the business reality and for a bootstrapped founder, the reality is that revenue is the only guaranteed funding source.

Why Bootstrapped Modeling Is Fundamentally Different

Here is where most explanations get superficial. The difference is not just that you project less aggressive growth. The difference is that the logic of every decision changes.

In a venture-backed company, a bad quarter triggers a fundraise conversation. In a bootstrapped company, a bad quarter triggers a survival conversation. That asymmetry reshapes how you model expenses, when you hire, what growth rate you can afford, and how you think about risk.

Entrepreneurship researcher Amar Bhidé documented that most successful small businesses grow through internally generated cash, not external capital and that this constraint forces a different kind of operational discipline from day one. The bootstrapped financial model is the formal expression of that discipline.

Three implications flow from this:

Cash timing matters more than profit. A business can be profitable on paper revenue recognized, invoices sent and still fail because customers pay in 45 days while suppliers require payment in 15. Profit is an accounting measure. Cash is the reality. A bootstrapped model must be built on cash basis, not accrual, especially in the first 18 months.

Conservative assumptions are not pessimism they are precision. Venture-backed projections build upward from market size assumptions. Bootstrapped projections build forward from actual customer conversations, closed contracts, and validated demand signals. As SaaS metrics pioneer David Skok has noted, the relationship between customer acquisition cost and lifetime value determines whether growth is sustainable and in a bootstrapped company, you must know this ratio before you spend a dollar on scaling.

The model is a decision engine, not a reporting document. The goal is not to produce accurate projections for their own sake. The goal is to answer one recurring question: Can we afford this next step using only the money we earn?

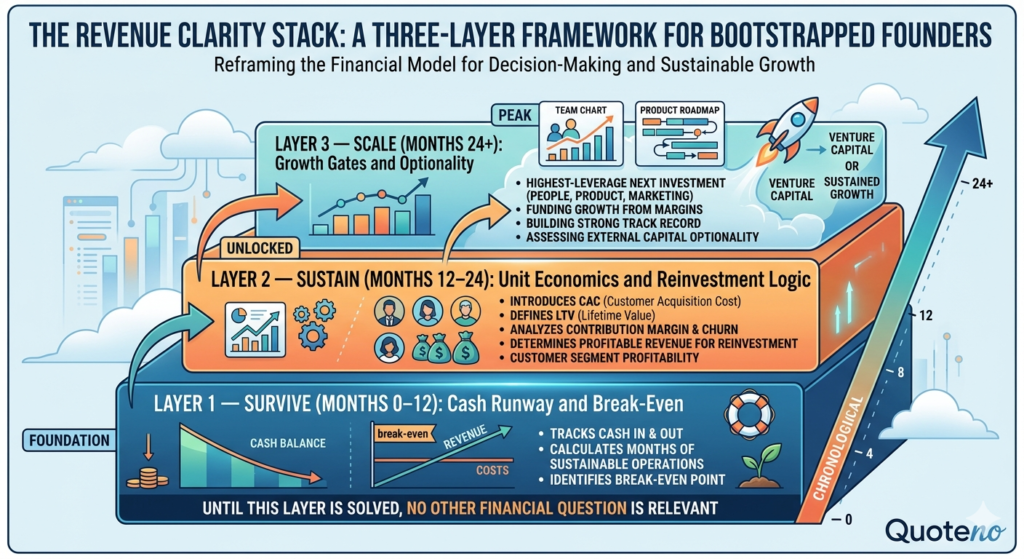

The Revenue Clarity Stack: A Three-Layer Framework for Bootstrapped Founders

Most guides present bootstrapped financial modeling as a set of spreadsheet components. That approach is accurate but incomplete. It tells you what to build, not why each layer matters or what decision it enables.

The Revenue Clarity Stack reframes the model as three nested layers of financial visibility, each unlocking a different category of founder decision:

Layer 1 — Survive (Months 0–12): Cash Runway and Break-Even

The first question is the only one that matters at the start: How long can we sustain operations on current resources? This layer tracks cash in, cash out, and the number of months until the balance reaches zero. It also identifies the exact revenue level at which the business covers its own costs — the break-even point.

Until this layer is solved, no other financial question is relevant.

Layer 2 — Sustain (Months 12–24): Unit Economics and Reinvestment Logic

Once survival is confirmed — meaning the model shows positive cash flow or a clear path to it — the second question becomes: Which revenue is profitable enough to reinvest in? This layer introduces CAC, LTV, contribution margin, and churn. It tells the founder which customer segments generate durable economic value versus which ones consume more in service costs than they return in revenue.

Layer 3 — Scale (Months 24+): Growth Gates and Optionality

Only founders who have solved layers one and two reach this stage from a position of strength. Layer three answers: What is the highest-leverage next investment — in people, product, or marketing — that our margin structure can fund without threatening layer-one survival? It also determines whether the company has built a financial track record strong enough to attract external capital on favorable terms, should the founder choose that path.

Most competitors jump immediately to layer three scenario planning, headcount modeling, investor positioning without building the foundation. The Revenue Clarity Stack enforces the correct sequence.

The Five Core Components of a Bootstrapped Financial Model

A functional bootstrapped model integrates five interconnected sections. These are not independent spreadsheets — they feed each other. Revenue assumptions flow into cash flow. Cash flow determines runway. Runway constrains hiring. Hiring affects expenses, which loops back into break-even.

1. Revenue Forecasting

Start with the smallest defensible number, then build upward from validated assumptions.

The driver-based formula most bootstrapped founders use:

Monthly Revenue = (New Customers Acquired × Average Revenue Per Customer) − (Churned Customers × Average Revenue Per Customer)

For a SaaS startup charging $50/month that acquires 20 new customers monthly with 3% monthly churn:

- Month 1: 20 customers × $50 = $1,000

- Month 6 (with compounding churn): approximately 110 active customers × $50 = $5,500

- Month 12: approximately 200 active customers × $50 = $10,000

The churn adjustment is critical. Many founders model gross customer additions without subtracting churn, which overstates revenue by 15–40% in the first year and creates a false sense of financial security.

For service businesses, replace the subscription formula with a capacity-based model: how many clients can your team serve simultaneously, at what average engagement value, with what average contract length?

2. Expense Modeling

Break expenses into two categories that behave differently as revenue changes:

| Expense Type | Examples | Behavior | Modeling Rule |

|---|---|---|---|

| Fixed costs | Salaries, SaaS tools, rent | Static regardless of revenue | List every line item; review monthly |

| Variable costs | Payment processing, COGS, shipping | Scale with revenue or customer count | Express as % of revenue or $ per unit |

One common error: treating founder compensation as zero to make the model look better. This creates a false picture of sustainability. If the business cannot fund a basic founder salary within 12–18 months, the model is not yet viable — and that is important information, not something to hide from yourself.

3. Cash Flow Forecasting

This is the most critical section of any bootstrapped model. The cash flow statement tracks the actual timing of money moving in and out of the bank account — not when revenue is recognized, but when cash is received.

A business that invoices $30,000 in March but collects it in May has a March cash flow of near-zero, even if the P&L shows $30,000 in revenue. This timing gap has ended businesses that appeared healthy on paper.

Build a rolling 12-month cash flow forecast with:

- Opening cash balance each month

- Cash receipts (actual collection dates, not invoice dates)

- Cash disbursements (vendor payment dates, payroll dates, tax deadlines)

- Closing cash balance each month

The closing balance in any month is your early warning system. When it drops below your minimum cash buffer threshold — a floor you set and never violate — it triggers a response protocol before the crisis, not during it.

Minimum cash buffer benchmark: Most experienced bootstrapped founders maintain a floor equal to 3 months of fixed operating expenses. Below that threshold, every discretionary expense is paused until the buffer is restored.

4. Break-Even Analysis

Break-even is the revenue level at which total revenue equals total costs — neither profit nor loss. For a bootstrapped founder, knowing this number precisely converts growth from an emotional goal into a mathematical target.

Break-even formula:

Break-Even Customers = Fixed Monthly Costs ÷ Contribution Margin Per Customer

Where: Contribution Margin Per Customer = Revenue Per Customer − Variable Cost Per Customer

Example: A bootstrapped SaaS company with $12,000 in monthly fixed costs and a $50 subscription price with $8 in variable costs per customer:

- Contribution margin = $50 − $8 = $42 per customer

- Break-even = $12,000 ÷ $42 = 286 customers

That number — 286 customers — is not a forecast. It is a decision gate. The founder knows exactly what the model requires before any discretionary hiring or marketing scaling is justified.

5. Key Performance Metrics Dashboard

Bootstrapped startups track fewer metrics than venture-backed companies, but they track them more carefully and more frequently. The survival-critical metrics:

| Metric | What It Tells You | Healthy Benchmark |

|---|---|---|

| Cash Runway | Months of operation at current burn rate | Minimum 6 months; target 12+ |

| Monthly Burn Rate | Cash spent per month net of revenue | Must be declining as revenue grows |

| MRR Growth Rate | Month-over-month revenue momentum | 5–15% monthly in early stages |

| Churn Rate | % of customers lost monthly | Under 2% monthly for SaaS; 0% for services |

| LTV:CAC Ratio | Revenue value per customer vs. cost to acquire | Minimum 3:1 for sustainable model |

| Gross Margin | Revenue minus direct cost of goods/services | 70%+ for SaaS; 40–60% for services |

| Payback Period | Months to recover CAC from gross profit | Under 12 months for bootstrapped model |

Jason Lemkin, the SaaStr founder and one of the most widely cited voices in SaaS growth, has consistently noted that revenue-first thinking prevents founders from making growth bets on unvalidated demand. That principle is the foundation of every metric in this table: measure what you’ve earned, not what you hope to earn.

The Profitability Trap: Why a Profitable Business Can Still Fail

This is the most under-explained failure mode in bootstrapped startups, and no competitor page addresses it with enough clarity to be useful.

A business can be profitable revenue exceeds expenses in the accounting period — and still run out of cash. This happens when there is a timing mismatch between when revenue is earned and when cash is received, or between when expenses are incurred and when they must be paid.

The Profitability Trap Diagnostic run this monthly:

- Open your P&L. Is net income positive? ✓ or ✗

- Open your cash flow statement. Is operating cash flow positive? ✓ or ✗

- If #1 is ✓ but #2 is ✗ — you are in the Profitability Trap.

The gap between those two numbers is caused by three structural forces:

- Accounts receivable lag: Customers owe you money but haven’t paid yet

- Inventory or prepaid expense buildup: You paid for inputs before you earned revenue from them

- Deferred revenue mismatch: In SaaS, annual subscriptions paid upfront may appear as revenue monthly while cash came in once

The fix is not to ignore accrual accounting that matters for tax purposes but to build your operational decision-making on cash flow, not P&L. The P&L tells you if the business model works. The cash flow statement tells you if the business survives.

As Pam Prior, a Forbes Finance Council contributor, has noted, the distinction between managing a budget and managing working capital is precisely where most founders lose their footing.

Bootstrapped vs. VC-Backed Modeling: When the Logic Diverges

The comparison is not about which approach is superior. It is about understanding that the two models answer different questions.

A VC-backed model is optimized to answer: How do we grow market share fast enough to justify a higher valuation in the next funding round? It can tolerate years of negative cash flow because external capital fills the gap.

A bootstrapped model is optimized to answer: How do we grow without ever needing to beg for capital? Every expansion decision must be funded by existing margin. This is not a constraint — it is a competitive advantage. Founders who master it operate with full ownership, zero dilution, and the negotiating power that comes from not being desperate.

The table below shows where the logic diverges in practice:

| Decision | VC-Backed Approach | Bootstrapped Approach |

|---|---|---|

| When to hire | When you can make the case to investors | When recurring revenue covers salary for 3–6 months |

| When to expand marketing | When capital is available | When LTV:CAC exceeds 3:1 and payback is under 12 months |

| When to enter a new market | Strategic timeline driven by board | Only when core market generates margin surplus |

| When to build new features | Product roadmap guided by growth metrics | Only when existing revenue can absorb dev cost |

| How to handle a bad quarter | Extend runway via bridge round | Immediately reduce discretionary spend to runway floor |

Industry-Specific Modeling: SaaS vs. Services vs. E-Commerce

Every competitor article uses a SaaS example. Real bootstrapped founders operate across business models, and each has distinct modeling requirements.

SaaS (Software as a Service): The primary financial driver is MRR, shaped by acquisition and churn. The most important dynamic to model is the J-curve of customer acquisition costs you spend money acquiring customers before they generate enough recurring revenue to recover that spend. The payback period is therefore the most critical metric in the first 18 months. Target under 12 months for a sustainable bootstrapped SaaS.

Service businesses (consulting, agencies, freelance): Revenue is capacity-constrained, not demand-constrained. The model must track utilization rate what percentage of billable hours are actually billed. A consulting firm with four consultants at 60% utilization earns 40% less than it could at full capacity. The financial model must project the utilization growth path, not just headcount additions.

E-commerce and physical products: Cash flow timing becomes especially complex due to inventory cycles. A founder who orders $50,000 in inventory in January, receives it in February, sells it in March, and collects payment in April has a 90-day cash conversion cycle. The bootstrapped model must account for this lag explicitly, or the founder may run out of cash during a period of strong sales.

Scenario Planning: The Three-Scenario Rule

A bootstrapped financial model built on a single forecast is not a model — it is a wish. Real financial clarity comes from running three scenarios simultaneously:

Base case: Revenue grows at the modest, validated rate based on recent performance. Expenses grow proportionally. This is the most likely outcome and the one you manage toward.

Pessimistic case (stress test): Revenue is 30–40% lower than base. What happens to runway? At what month does the cash balance hit the minimum buffer floor? What specific cost cuts would be required to extend survival by 90 days? This scenario defines your response protocol before you need it.

Optimistic case (capacity check): Revenue is 30–40% higher than base. Can operations handle it? Does your customer success process break? Does fulfillment capacity overflow? Rapid growth that exceeds operational capacity destroys quality and customer retention and in a bootstrapped company, those customers are the only investors you have.

According to the Abacum Capital Markets Study (2025), startups that prepare three or more financial scenarios secure funding at nearly twice the rate of those using a single projection not because investors prefer bootstrapped companies that model scenarios, but because multi-scenario thinking signals the kind of financial discipline that makes any business fundable.

When Your Bootstrapped Model Becomes Your Investor Pitch

Many founders bootstrap as a phase, not a permanent choice. They self-fund to prove the model, then raise external capital from a position of strength with real customers, real revenue, and a financial history that eliminates speculation.

A well-maintained bootstrapped financial model is the most compelling artifact you can bring to that conversation, because it demonstrates precisely what most pre-revenue startups cannot: that the unit economics actually work under real-world conditions.

What investors look for in a bootstrapped founder’s model:

- Actual historical cash flow data, not projections alone

- LTV:CAC ratio validated by real customer behavior

- Churn rate measured over at least 6–12 months

- Break-even already achieved or within a defined, funded timeline

- A conservative base-case forecast with documented assumptions

Founders who negotiate from this position with leverage rather than desperation routinely achieve better terms, higher valuations, and more investor confidence than teams whose models are entirely speculative.

Tools for Building Your Bootstrapped Financial Model

| Tool | Best For | Stage | Cost |

|---|---|---|---|

| Google Sheets | Simple early-stage models | Pre-revenue to $10K MRR | Free |

| Microsoft Excel | More complex modeling, offline first | Any stage | Low |

| Finmark | Scenario planning, visual dashboards | $10K–$500K MRR | Paid |

| Mosaic | Strategic finance, team collaboration | Growth stage | Paid |

| Pry | Driver-based modeling, SaaS focus | $5K–$200K MRR | Paid |

| QuickBooks | Actuals tracking, tax integration | Any stage | Paid |

| Baremetrics / ChartMogul | SaaS MRR and churn tracking | SaaS-specific | Paid |

For most bootstrapped founders in the first 12–18 months, Google Sheets or Excel is not just adequate it is often preferable. Complex modeling tools introduce setup overhead that pulls attention away from building the business. Simplicity is a feature, not a limitation, when cash clarity is the goal.

The most important principle: a model you actually use beats a sophisticated model you avoid updating. Update your cash flow forecast weekly during tight periods; monthly when the business is healthy.

The Most Common Bootstrapped Modeling Mistakes (And How to Avoid Them)

1. Building from top-down market assumptions. “If we capture 1% of a $1B market…” is a venture pitch logic. Bootstrapped models must build from validated customer acquisition capacity how many customers can you realistically close in the next 30 days?

2. Ignoring cash timing. Revenue recognized is not cash received. Model the actual collection date, not the invoice date.

3. Excluding founder compensation. The model must sustain the founder. If it cannot, the model is not yet complete — not “more profitable.”

4. Forgetting churn. Even 3% monthly churn eliminates over 30% of your customer base within a year. A model that ignores churn overstates revenue materially.

5. Treating the model as a quarterly exercise. A bootstrapped model should be reviewed monthly — weekly if the business is in or near the survival zone.

6. Building 20-tab complexity in month one. A five-section model reviewed consistently outperforms a 20-tab model that never gets updated because it is too cumbersome to maintain.

Frequently Asked Questions

What is startup booted (bootstrapped) financial modeling?

Startup booted financial modeling is the practice of building financial forecasts for a startup that runs entirely on internally generated revenue, founder capital, and early customer payments with no assumed external investment. The model prioritizes cash survival, break-even discipline, and unit economics over growth-at-any-cost projections.

How is a bootstrapped financial model different from a VC-backed model?

The fundamental difference is the funding assumption. A VC-backed model assumes future capital rounds will fill any cash gap. A bootstrapped model assumes revenue must fund every operational decision. This changes the logic of when to hire, when to expand, and how to define healthy growth.

What is cash runway and why does it matter for bootstrapped startups?

Cash runway is the number of months a startup can sustain operations at its current burn rate using existing cash reserves. For bootstrapped founders, runway is the most critical metric because there is no external capital to extend it. A minimum of 6 months of runway is the standard floor; 12 months provides operational freedom.

What metrics should a bootstrapped startup track?

The survival-critical metrics are: cash runway, monthly burn rate, MRR growth rate, monthly churn rate, LTV:CAC ratio, gross margin, and payback period. These are not investor metrics they are operating metrics that determine daily decisions.

Can a bootstrapped startup attract investors later?

Yes and often on better terms than pre-revenue startups. A bootstrapped company with validated unit economics, real customers, and a 12+ month financial history removes the speculation from every investor conversation. Founders who raise from a bootstrapped position tend to negotiate higher valuations and better terms because they are not raising from necessity.

What tools do bootstrapped founders use for financial modeling?

Most early-stage bootstrapped founders start with Google Sheets or Excel. As the business grows, tools like Finmark, Mosaic, or Pry offer more automation, scenario planning, and dashboard visibility. SaaS-specific founders often pair their financial model with ChartMogul or Baremetrics for real-time MRR and churn tracking.

How often should a bootstrapped financial model be updated?

The cash flow forecast should be updated weekly during high-risk periods (low runway, high uncertainty) and at minimum monthly during stable periods. Revenue forecasts and expense assumptions should be reviewed and adjusted monthly as actual performance becomes available.

When should a bootstrapped startup hire its first full-time employee?

The standard threshold is when recurring revenue has consistently covered the new salary for at least 3 consecutive months not when you project it will. Hiring on projected revenue rather than actual revenue is one of the most common causes of cash crisis in bootstrapped startups.

Read also: J.P. Morgan bootstrap guide

- How Denver’s Outdoor Lifestyle Shapes Its Real Estate Market - July 20, 2026

- Modern Maintenance Solutions for Urban Commercial Buildings - July 19, 2026

- Sustainable Innovations Reshaping Commercial Construction - July 11, 2026