Auto loan refinancing replaces your existing car loan with a new one, ideally with more favorable terms. This new loan pays off your current balance and then continues with a different interest rate, new repayment length, or both. Many borrowers use refinancing to lower their monthly car payments, relieve financial stress, or take advantage of improved credit. Services like iLending help borrowers explore refinancing options and connect with lenders offering competitive rates.

Whether you are struggling to keep up with payments or simply want to pay less on your car each month, refinancing could provide valuable relief. It is also a popular option for those whose financial picture has changed since taking out their original vehicle loan, such as an improved credit score or a desire for different repayment terms.

Table of Contents

Key Takeaways

- Auto loan refinancing can lower your monthly payments by reducing your interest rate or improving your loan terms.

- The current interest rate environment, your credit score, and the loan term all influence the refinancing rate you are offered.

- Borrowers are saving significant amounts each month by refinancing at lower rates.

- Understanding the refinancing process helps you identify the right time and method to maximize savings.

The Impact of Interest Rates on Monthly Payments

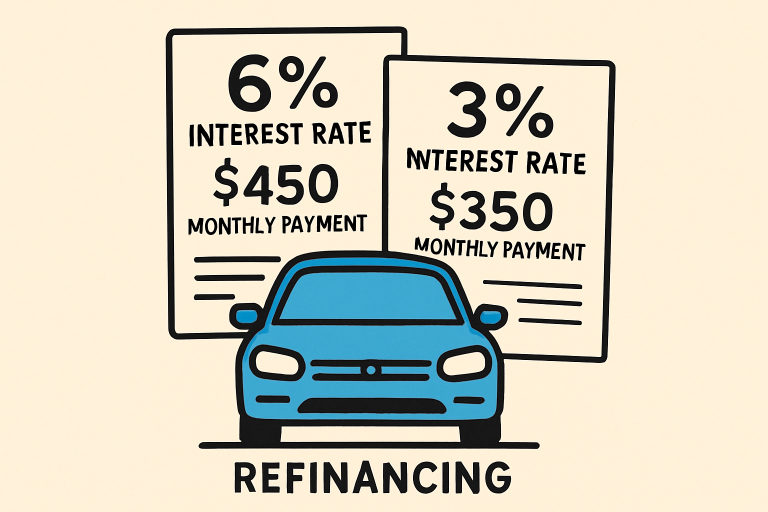

Interest rates are the largest factor affecting your monthly auto loan payment. When you refinance to a lower rate, the portion of your payment that goes toward interest decreases. This means more of your payment goes toward the principal, helping you pay down your loan faster and at a lower total cost. Conversely, a higher interest rate means you pay more each month and over the life of the loan. Understanding how rates work and their effect on your payment is critical.

If you locked in a car loan when rates were high, or your credit was less established, the difference refinancing can make to your monthly budget can be dramatic. Even a one- or two-point reduction in your rate may save you hundreds or thousands over the life of your loan.

Recent Trends in Auto Loan Refinancing

Auto loan refinancing has become increasingly popular, particularly as interest rates fluctuate and borrowers look for ways to save. According to Experian’s Q2 2025 State of the Auto Finance Market report, consumers who refinanced their auto loans during this period experienced meaningful savings. They were able to cut their average interest rate from 10.45 percent to 8.45 percent, resulting in approximately $71 less in monthly payments. This trend highlights that more consumers are becoming aware of the tangible benefits refinancing can offer.

Lenders have responded to increased demand by expanding their refinancing offerings. For consumers, this means more competition between providers and potentially better deals.

Factors Influencing Refinancing Rates

Several factors affect the rate and terms you may be offered when you refinance your auto loan:

- Credit Score: Borrowers with higher credit scores are typically eligible for lower interest rates. If your credit has improved since your original car loan, you may qualify for much better terms during refinancing.

- Loan Term: The length of your new loan also plays a major role. Shorter loan terms often result in lower rates but can raise monthly payment amounts, while longer terms may reduce monthly payments but increase the total interest paid.

- Market Conditions: Prevailing economic factors, such as changes in the Federal Reserve’s interest rate policy or general shifts in auto lending, directly impact the rates you see offered by various lenders.

Some lenders may also evaluate your car’s age and mileage, your debt-to-income ratio, and your employment history before quoting a refinancing rate. Each of these elements can raise or lower your offered rate.

When to Consider Refinancing

Timing is crucial in refinancing. You might want to consider refinancing if:

- Rates have dropped since you initially financed your vehicle, making it possible to secure a better deal now.

- Your credit score has improved, increasing your eligibility for lower rates and better terms.

- You need to adjust your loan term by extending it to lower your monthly payment or shortening it to pay your debt off faster.

Other events, such as changes in income or expenses, might prompt you to explore refinancing as well. Carefully reviewing your current loan against lender offers can reveal whether refinancing is likely to result in substantial savings or better fit your monthly budget.

Potential Savings from Refinancing

The potential for savings when refinancing your auto loan can be considerable. Refinancing in 2025 helped borrowers cut average monthly payments by $71 and reduce total loan costs by more than $1,300, according to recent reports. The exact savings you realize depend on your current interest rate, the new rate you can secure, the loan balance, and any applicable refinancing fees.

Before moving ahead, factor in any costs charged by your current or new lender. Some loans include prepayment penalties or refinancing fees. Make sure that the benefits of a lower monthly payment and overall interest savings outweigh these costs to justify refinancing.

Steps to Refinance Your Auto Loan

- Assess Your Current Loan: Gather information on your current loan’s balance, interest rate, repayment term, and any early payoff conditions.

- Check Your Credit Score: Knowing your credit score helps you anticipate the rates you may be offered. Improving your credit before applying can help you secure better terms.

- Shop Around: Compare interest rates, fees, and terms from multiple lenders instead of settling for the first offer you receive. This can help you find the most competitive deal.

- Calculate Potential Savings: Use online auto loan calculators to model potential savings on your monthly payment and total interest expense.

- Review Terms Carefully: Examine all loan paperwork for hidden fees, prepayment penalties, or other binding conditions before committing to refinance.

Following this step-by-step process increases your chances of getting the most from refinancing and maximizing your monthly or long-term savings.

Final Thoughts

Auto loan refinancing, when approached strategically, can put money back in your pocket and help you realize better control over your monthly budget. By understanding how rates affect payments, monitoring industry trends, and strengthening your financial profile, you can unlock meaningful savings through refinancing. Take time to research your options and compare offers to ensure your next auto loan delivers both immediate and long-term financial benefits.

- Managing Chronic Pain with Innovative Therapies - April 4, 2026

- Reducing Damage from Plumbing Emergencies: Proactive Strategies for Homeowners - April 1, 2026

- Understanding Your Rights After A Personal Injury In Texas - March 30, 2026